Markets: Stability with mixed signals

Week of April 27 to May 1

Stable rates, persistent inflation, and uneven growth define the week

Markets reflect stability in monetary policy, but with increasing divergence in growth and inflation. The geopolitical backdrop continues to pressure expectations and limit global economic visibility.

United States

The Fed held rates at 3.5%–3.75% with an 8–4 split, the largest since 1992. GDP grew 2.0%, driven by AI investment and government spending, but consumption is slowing. Confidence improved, though inflation pressures persist.

Europe

The ECB and BoE held rates but warned of inflation risks from energy. Inflation rose to 3%, while Germany’s economy grew 0.3%, reflecting modest expansion close to stagnation.

Japan

The BoJ kept rates at 0.75% amid internal division over inflation concerns. Retail sales rose 1.7%, driven by the automotive sector, signaling a gradual recovery in consumption.

China

Manufacturing PMI reached its highest level in a year. However, rising input costs from energy and metals are pressuring margins and the sustainability of growth.

Argentina

Fitch Ratings and Moody’s maintain a cautious outlook, highlighting risks from persistent inflation, institutional weakness, and reliance on fiscal adjustment.

Brazil

The central bank cut rates to 14.50%, supported by lower-than-expected inflation (4.37%). The easing cycle continues despite global uncertainty.

Mexico

GDP declined 0.8% in 1Q, with broad-based weakness. Despite record exports (+27.7%), external strength has yet to translate into domestic growth.

“All intelligent investing is value investing. Acquiring more than you are paying for. You must value the business in order to value the stock.” – Charlie Munger

KEY UPCOMING EVENTS

- In the United States, Services PMI will be released on 05/05

- In the United States, nonfarm payrolls will be released on 05/08

Monitor:

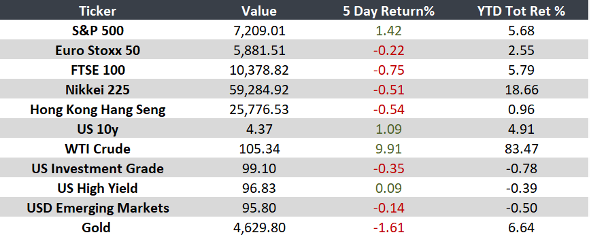

Note: Returns as of April 30th at closing.