Markets: inflation, energy, and mixed signals

Week of April 6–10

Inflation, energy dynamics, and geopolitical tensions shape the global markets outlook.

Markets are navigating a complex environment, with inflationary pressures tied to energy and ongoing geopolitical tensions weighing on growth prospects. The U.S. shows mixed signals, while Europe and emerging markets reflect slowing activity.

United States

Inflation rises on energy and the services PMI declines amid cost pressures. GDP is revised lower. The Fed keeps rate cuts on the table should inflation moderate or labor market conditions soften.

Europe

Producer inflation slows and consumption remains resilient. However, industrial orders and production in Germany point to economic stagnation.

Japan

Producer prices increase due to higher operating costs, reflecting pressure across industrial and transportation sectors.

China

Consumer inflation moderates, but producer prices rise driven by energy and raw materials, highlighting persistent cost pressures.

Argentina

Industrial production declines sharply across most sectors, reflecting broad-based economic weakness.

Brazil

Inflation rises, driven by fuel and food prices, amid global energy pressures.

Mexico

Inflation remains elevated and Banxico projects gradual convergence. Investment declines amid uncertainty and tight financial conditions.

“The longer you can extend your time horizon the less competitive the game becomes.” – Howard Marks

Key upcoming events

- In the United States, the Producer Price Index (PPI) will be released on 04/14

- In the United States, Industrial Production data will be released on 04/16

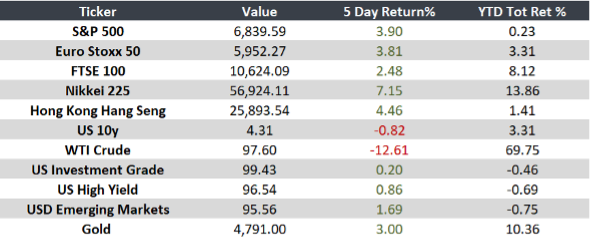

Monitor