Markets Between Resilience and Inflationary Pressure

Global Weekly Outlook

Week of June 8–12

Persistent inflation and geopolitical tensions continue to shape markets

The week was marked by higher inflation across several economies, energy-related pressures stemming from the Middle East conflict, and mixed growth signals. Despite these challenges, some sectors continue to demonstrate resilience, while investors remain focused on monetary policy decisions.

United States

Inflation rose to 4.2%, while PPI reached its highest level since 2022. However, home sales remained strong, and SpaceX completed the largest IPO in history.

Europe

The ECB raised rates to 2.25% and revised its inflation outlook higher. Germany saw inflation moderate, while the UK recorded its first economic contraction since August.

Japan

GDP exceeded expectations, supported by consumer spending and exports. However, producer prices rose 6.3%, reflecting the impact of higher energy costs.

China

Inflation remained stable, but producer prices reached their highest level since 2022. Energy and commodity costs continue to pressure industrial margins.

Argentina

Inflation edged up to 33.6% year-over-year in May. Despite the increase, it remains well below levels seen in recent years.

Brazil

Inflation reached 4.72%, exceeding expectations and marking its highest level since September, driven by food and energy prices.

Mexico

Inflation returned to Banxico’s target range and producer prices moderated. However, automotive production declined, although exports continued to grow.

“You make most of your money in a bear market, you just don’t realize it at the time.” — Shelby Cullom Davis

Key Upcoming Events

- In the United States, industrial production data will be released 06/15

- In the United States, the FED monetary policy decision will be released on 06/17

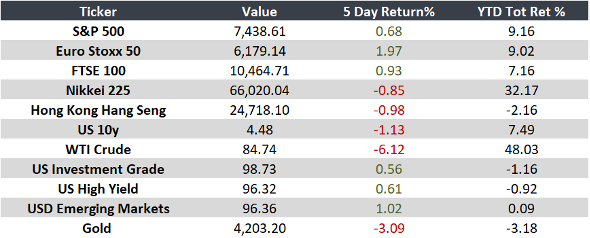

Monitor:

Note: Returns as of 10 AM ET.