Global Weekly Overview

Week of May 11 to May 15

A week marked by elevated inflation and mixed growth signals

Recent data point to a backdrop of persistent inflation driven by energy and geopolitical tensions. Despite this, consumption remains resilient in some economies, while growth is losing momentum in others.

United States

Inflation rises to 3.8% and PPI to 6.0%, driven by energy. Consumption remains resilient, but housing is slowing. Markets scale back rate cut expectations and increase the probability of hikes.

Europe

Eurozone GDP grows 0.8%, impacted by energy. Germany faces rising inflation and costs, while the UK surprises with stronger growth, although investment remains weak.

Japan

Producer prices rise to 4.9%, the highest since 2023. Energy costs are increasing inflationary pressures and influencing BoJ policy.

China

Inflation rises to 1.2% and PPI to 2.8%, driven by energy. Cost pressures could pass through to global prices despite weak food demand.

Argentina

Inflation slows to 32.4% year-over-year. While still elevated, it shows a moderating trend compared to previous levels.

Brazil

Inflation rises to 4.39%, driven by food and transportation. The figure remains below expectations, reflecting contained pressures.

Mexico

Employment grows but remains below required levels. Industrial activity contracts, while the automotive sector stands out as a key driver due to export strength.

“Patience is not passive; it is concentrated strength.” – Bruce Lee

KEY UPCOMING EVENTS

- In the United States, the FED minutes will be released on 05/20

- In the United States, employment related data will be released on 05/21

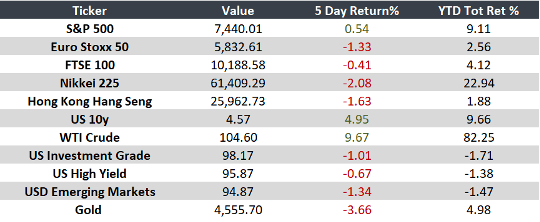

Monitor:

Note: Returns as of 10 AM ET.