Week of February 23–27

Markets are balancing solid earnings, evolving trade policy, and diverging inflation trends across regions. While growth remains resilient in some economies, policy uncertainty and valuation levels continue to guide investor positioning.

United States

The Supreme Court struck down “emergency” tariffs due to lack of Congressional approval. The Administration introduced a new 10% global tariff. PPI rose 0.5% in January, core at 3.6%. Earnings remain strong, while jobless claims suggest a steady labor market and a Fed on hold.

Europe

Eurozone inflation eased to 1.7%, below the ECB target range, with core at 2.2%. Germany’s inflation moderated to 1.9%, though services remain elevated. Business confidence improved, but consumer sentiment softened amid geopolitical uncertainty.

Japan

The leading economic index reached its highest level since May 2024, supported by labor strength. Services inflation rose 2.6%, reflecting wage pressures. Consumer sentiment weakened due to higher costs and interest rates.

China

The IMF urged China to shift toward consumption-led growth and reduce industrial subsidies, aiming to address external imbalances following record trade surpluses.

Argentina

Economic activity rose 3.5% year-over-year, led by agriculture and mining. Retail sales increased 16.1% nominally, though real consumption declined due to inflation pressures.

Brazil

Brazil posted a primary surplus below expectations, as spending growth outpaced revenue gains, adding pressure to fiscal balance targets.

Mexico

Inflation rose to 3.92% in early February, with core easing slightly. Economic activity expanded 3.3% in December, but unemployment increased to 2.7%, with over 700,000 jobs lost in January.

“Buy a stock the way you would buy a house. Understand and like it such that you’d be content to own it in the absence of any market.” – Warren Buffett

Key upcoming events

- In the United States, manufacturing PMI will be released on 03/02

- In the United States, nonfarm payrolls will be released on 03/05

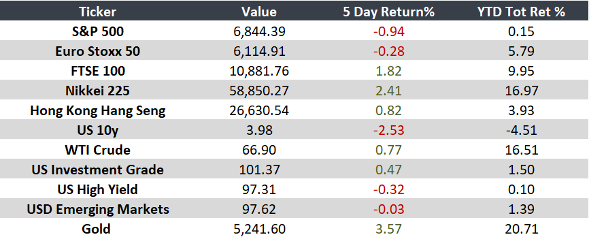

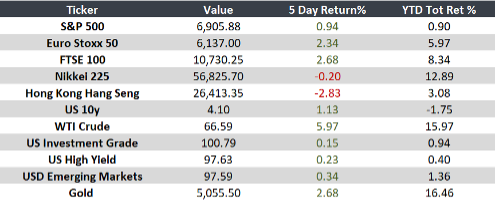

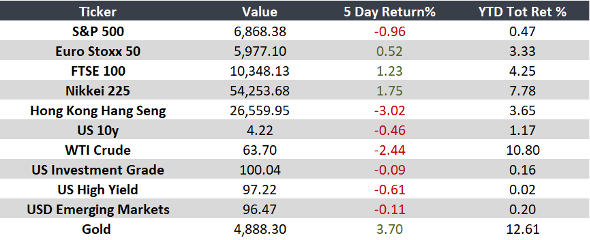

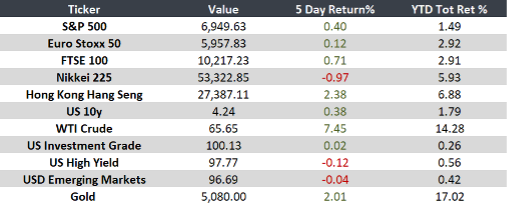

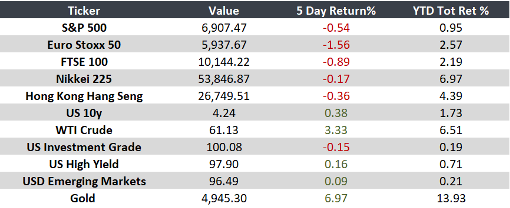

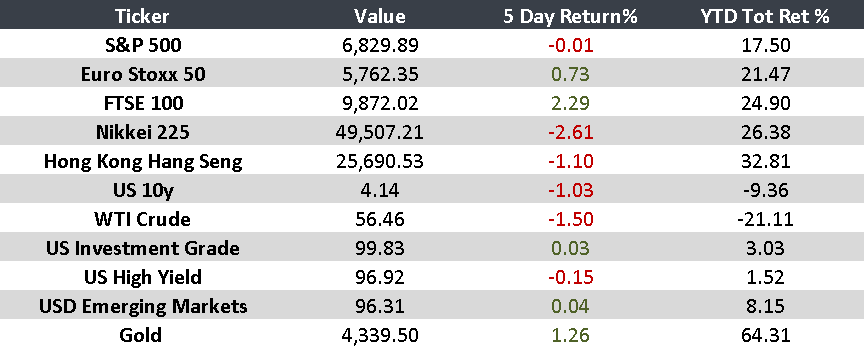

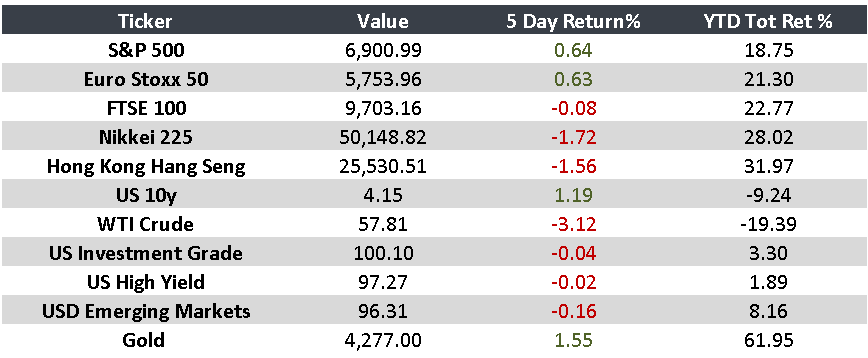

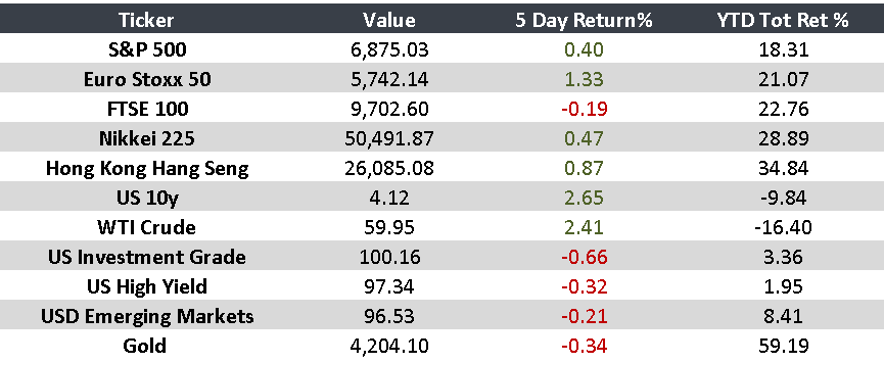

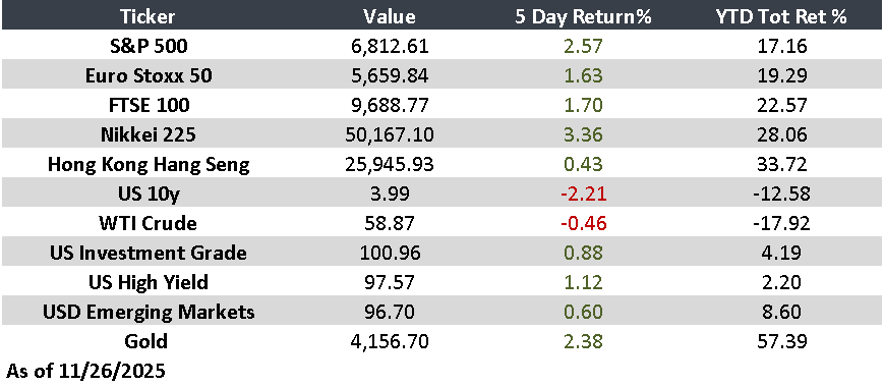

Monitor