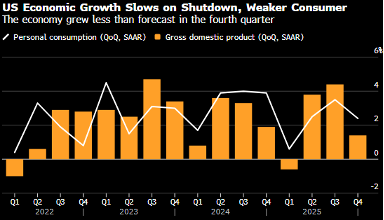

The U.S. economy grew at a 1.4% annualized rate in the fourth quarter of 2025, below expectations, as the government shutdown weighed on spending and exports. For the full year, growth came in at 2.2%, down from 2.8% in 2024.

Meanwhile, core inflation rose to 3% year over year in December, remaining above the Federal Reserve’s target.

Private demand analysis

Although the headline GDP figure was weak, private demand showed resilience: final sales to private domestic purchasers increased 2.4% and private investment rose 3.8%. The main drag came from federal government spending.

With inflation still elevated, the Fed is likely to maintain a cautious stance before considering further rate cuts.

Implications

At the same time, core inflation reached 3%, still above the Federal Reserve’s target. While the headline growth figure was soft, private demand and investment showed resilience. The overall backdrop suggests the Fed will remain cautious in the months ahead.

Source: Bureau of Economic Analysis, Bloomberg