Week of stable rates and mixed signals in manufacturing

November 3–7

Markets reflected a week of steady interest rates, weaker manufacturing data, and resilience in services. In the United States, the government shutdown remains unresolved, while year-end spending shows a more moderate tone compared with 2024.

United States:

Concerns over AI valuations drove market sentiment. Manufacturing activity declined, but the services sector rebounded. The government shutdown set a new record, and year-end spending is expected to moderate.

Europe:

Eurozone manufacturing stalled due to a lack of new orders, although production continued to grow. The Bank of England kept its policy rate at 4%, as expected.

Asia:

In Japan, manufacturing posted its worst reading in more than a year, pressured by weak demand in autos and semiconductors. The services sector remained resilient despite a slower pace of new orders.

In China, manufacturing activity fell to its lowest level in six months. Services expanded but at the slowest pace since July, mainly due to weaker export demand.

Latin America:

In Brazil, the Central Bank held its key rate at 15%, the highest level since 2006, indicating caution amid persistent inflationary pressures.

In Mexico, Banco de México cut its policy rate to 7.25%, in line with expectations. September remittances fell 2.7% YoY, though they remain above $5 billion.

“The investor’s chief problem — and even his worst enemy — is likely to be himself.” — Benjamin Graham

Important Events:

- U.S. October inflation data will be released — November 13

- U.S. Producer Price Index (PPI) will be published — November 14

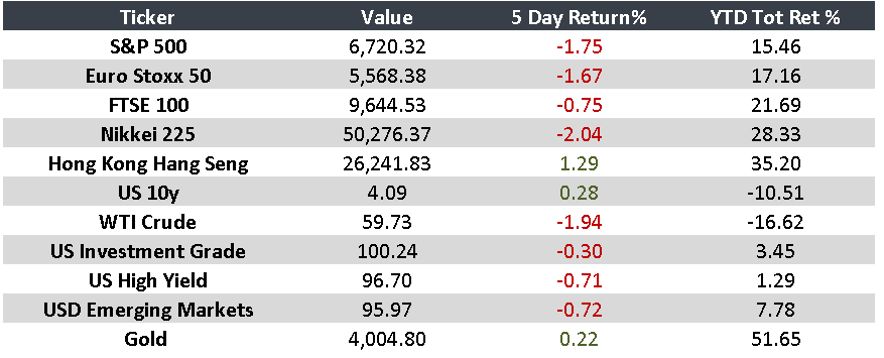

Monitor