U.S. core inflation cools further

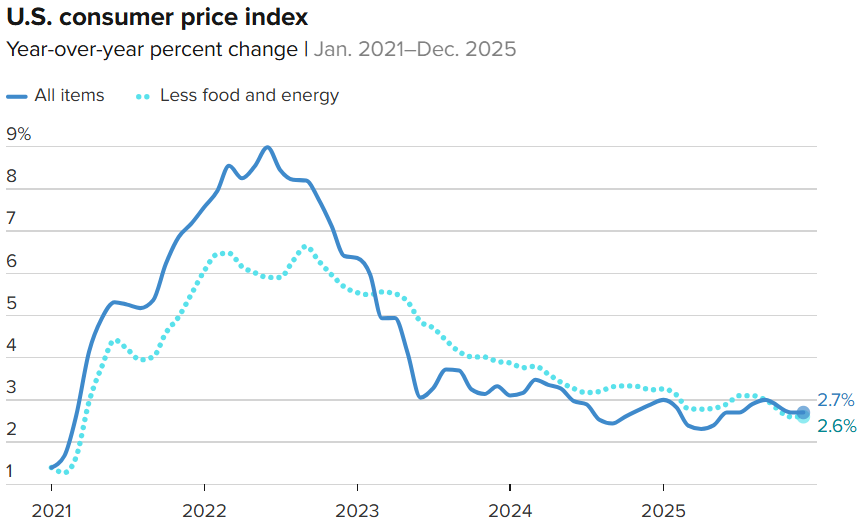

U.S. core inflation came in softer than expected in December, reinforcing the view that underlying price pressures are gradually easing. Core CPI rose just 0.2% month over month and 2.6% year over year, both below consensus, pointing to a continued normalization of inflation dynamics. Still, headline inflation remains at 2.7%, meaning price stability has not yet been fully restored.

What’s holding the Fed back is the composition of inflation. Housing costs, more than a third of CPI, continue to rise at an elevated pace, while services, recreation, and airfares remain sticky. Even as some goods show deflation, the Fed is still waiting for economic data and assessing the effects of previous cuts, limiting the case for near-term rate cuts. Markets now expect the Fed to remain on hold at least through the first half of the year.

Market Implications

- It reinforces the scenario of inflation slowing down, but too slowly to justify immediate interest rate cuts.

- Risks in the housing and services sectors reduce the likelihood of an accelerated monetary stimulus cycle.

- Makes upcoming inflation and labor data critical for market direction.

Source: CNBC with information from U.S. Bureau of Labor Statistics